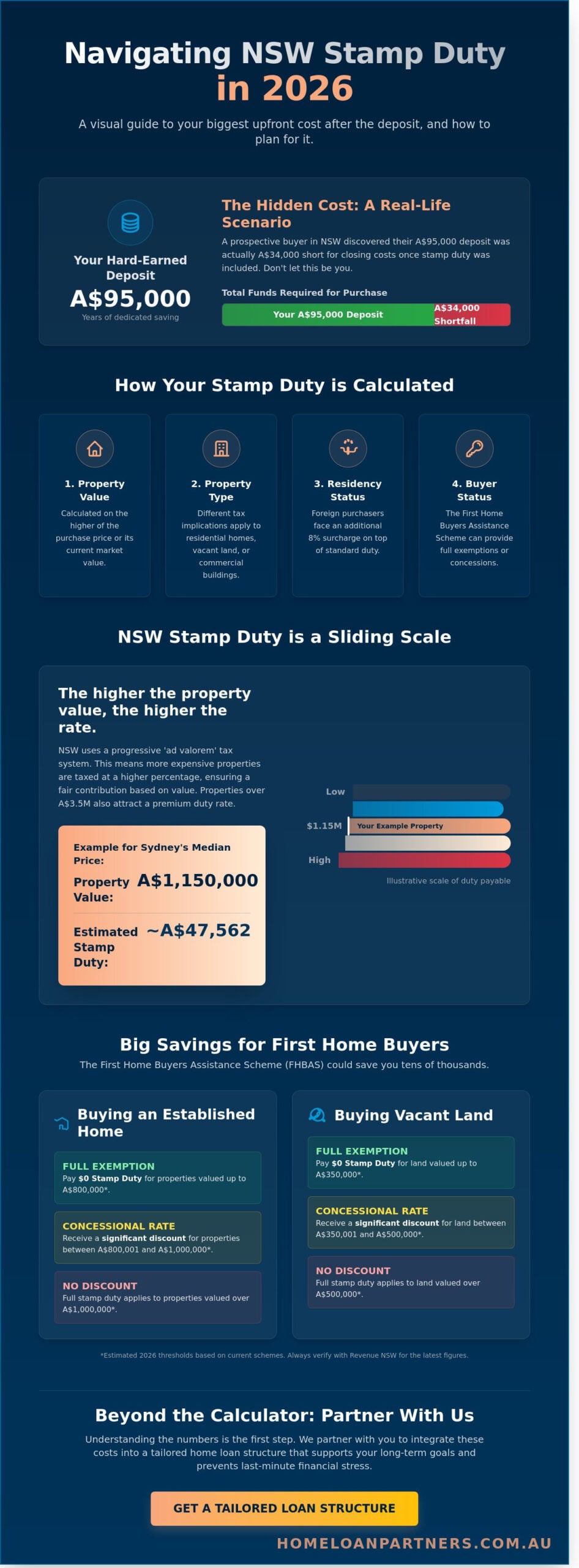

Last Tuesday, a prospective homeowner in New South Wales realized that their hard-earned A$95,000 deposit was actually A$34,000 short once the state’s transfer duty was factored into the closing costs. It’s a heavy realization that many Australians face when they discover the purchase price is only one part of the financial equation. You’ve likely spent years sacrificing to build your savings, and the fear of hidden taxes eating into your future home is completely valid. At The Home Loan Partners, we believe that clarity is the best cure for property-buying anxiety.

We’re here to help you move forward with confidence rather than guesswork. By using our stamp duty calculator nsw, you’ll gain an immediate, precise dollar figure for your 2026 property purchase. We’ll show you exactly how to navigate the latest government thresholds and identify if you qualify for first-home buyer concessions that could save you thousands. This guide breaks down the mandatory transfer duty, explores potential exemptions, and explains how to structure your loan so these costs don’t stall your journey to homeownership.

Key Takeaways

- Understand why transfer duty is your largest upfront cost after the deposit and how it impacts your total property budget.

- Use our stamp duty calculator nsw to receive an instant estimate tailored to your purchase price and specific property type.

- Discover if you qualify for the 2026 First Home Buyers Assistance Scheme to access full exemptions or significant concessions.

- Identify common pitfalls, such as the Foreign Purchaser Surcharge, to ensure your financial planning remains accurate and stress-free.

- Learn how we partner with you to integrate these costs into a tailored loan structure that supports your long-term homeownership journey.

What is NSW Stamp Duty and Why Does it Matter?

Buying a home is one of the most significant milestones you’ll ever reach. While most of your focus likely sits on saving for a deposit, it’s vital to account for transfer duty, which was previously called stamp duty. This state-mandated tax is collected by Revenue NSW and applies to the sale or transfer of land and property within the state. For most buyers, this tax represents the largest upfront cost outside of the deposit itself, often reaching tens of thousands of dollars.

Revenue NSW calculates this fee based on the higher of two figures: the actual purchase price or the current market value of the property. This ensures the tax remains fair and reflects the true worth of the asset. Because these costs can vary wildly based on the property’s location and price point, using a stamp duty calculator nsw helps you avoid any unexpected financial hurdles during the settlement process. We see our role as your partner in this journey, helping you translate these complex state regulations into a clear, manageable budget for your future home.

When is Stamp Duty Payable in NSW?

The law requires you to pay transfer duty within three months of the settlement date. While three months might seem like a generous window, most lenders require the duty to be paid at or before settlement to ensure the title can be legally transferred into your name. If you miss this deadline, Revenue NSW applies interest charges and potential late-payment penalties that can quickly inflate your total costs. Your solicitor or conveyancer typically acts as the intermediary here. They’ll calculate the exact amount, collect the funds from you or your lender, and ensure the payment reaches the government on time so your property rights are fully protected.

The Difference Between Fixed and Ad Valorem Rates

NSW uses a sliding scale to determine how much tax you owe, which means the percentage increases as the property value rises. Standard residential rates apply to most homes, but properties valued over A$3,505,000 as of the July 2024 thresholds attract a premium duty rate. An ad valorem tax is a percentage-based levy calculated according to the assessed value of the property. This system ensures that a modest apartment pays a lower rate than a sprawling estate. By using a stamp duty calculator nsw, you can see exactly where your potential home sits on this scale. This transparency allows us to build a tailored financial plan that secures your long-term stability without any hidden surprises.

How the NSW Stamp Duty Calculator Estimates Your Costs

Understanding your upfront costs is the first step toward a stress-free home purchase. A stamp duty calculator nsw processes four specific data points to give you a reliable figure. It starts with the property value. Revenue NSW typically uses the higher of the purchase price or the current market value to determine your tax liability. This ensures the state collects a fair amount based on actual asset worth.

Next, the tool considers the property type. Residential homes, commercial buildings, and vacant land all carry different tax implications. Your residency status is the third vital factor. While Australian citizens and permanent residents pay standard rates, foreign purchasers currently face an 8% surcharge on top of the base duty. Finally, the calculator applies 2026 concessions, such as the First Home Buyers Assistance Scheme, to see if you’re eligible for a discount or a full exemption.

Current Stamp Duty Brackets for 2026

NSW uses a sliding scale for transfer duty, which means the percentage you pay increases as the property value climbs. For the 2025/2026 financial year, the brackets are indexed to the Consumer Price Index. If you’re purchasing a median-priced residential property in Sydney for A$1,150,000, your estimated duty would be approximately A$47,562. This calculation includes a base amount plus a percentage of the value exceeding the nearest bracket threshold.

Bracket creep remains a significant factor for modern buyers. As property prices in regional hubs like Newcastle or Wollongong rise, more modest homes are pushed into higher tax tiers. It’s a hurdle that requires careful planning. We’ve seen many clients benefit from a tailored mortgage strategy that accounts for these shifting tax costs early in the savings journey.

Residential vs. Vacant Land Calculations

Buying land to build your dream home often results in a lower initial tax bill compared to buying an established house. This is because the duty is calculated solely on the land’s value at the time of settlement. For example, if you buy a block of land for A$400,000, your duty will be significantly lower than if you bought a finished home for A$900,000 on that same street.

- Full Exemptions: In 2026, first home buyers pay zero duty on vacant land valued up to A$350,000.

- Concessional Rates: A sliding scale of discounts applies to land valued between A$350,000 and A$450,000.

- Construction Loans: While you save on duty, remember that lenders often require a larger buffer for build contracts to cover unexpected price variations.

Choosing vacant land can be a smart way to enter the market with a smaller deposit. It allows you to put more of your hard-earned savings toward the actual construction rather than government fees. Our experts guide you through these thresholds to ensure you’re maximizing every available state incentive.

First Home Buyer Exemptions and Concessions in 2026

Buying your first home is a major milestone. The First Home Buyers Assistance Scheme (FHBAS) remains a cornerstone of support in 2026, providing either a total waiver or a significant discount on transfer duty for eligible buyers. This scheme is designed to help you enter the property market sooner by reducing the upfront cash you need to save. To qualify for these benefits, you must meet several specific criteria:

- Age and Status: You must be an individual at least 18 years old.

- Residency: At least one purchaser must be an Australian citizen or permanent resident.

- First-time Buyer: You and your partner cannot have owned or co-owned residential property in Australia before.

- Occupancy: You must move into the home within 12 months of settlement and live there for a continuous period of at least 12 months.

You don’t have to tackle the application paperwork alone. Your mortgage broker or solicitor typically manages the FHBAS application during the settlement process. They act as your guide, ensuring the correct codes are applied so you don’t overpay. Using a stamp duty calculator nsw early in your search helps you visualize these savings before you even make an offer on a property.

2026 Thresholds for First-Home Buyers

In 2026, the NSW Government maintains a clear line for financial support. Homes valued up to A$800,000 receive a full exemption, meaning you pay zero stamp duty. For properties priced between A$800,000 and A$1,000,000, a tapered concession applies. This sliding scale ensures the discount gradually reduces as the property value increases. For example, a buyer purchasing a A$600,000 property saves approximately A$22,000. A buyer at the A$800,000 cap saves roughly A$31,000, which is the maximum possible benefit under the current 2026 settings. These savings can be redirected toward your deposit or home improvements.

Shared Equity and First Home Buyer Schemes

Government shared equity programs often work alongside these exemptions to lower the entry barrier even further. In 2026, these initiatives allow the state to contribute to the purchase price in exchange for an equity share, which significantly reduces your loan size and monthly repayments. Because these schemes have specific price caps and income limits, they require careful coordination with your finance. We act as your expert partner to align these grants with your loan structure. Relying on a stamp duty calculator nsw ensures your budget accounts for every available dollar of support. Professional guidance is vital here, as missing a deadline or miscalculating a threshold can change your financial position by thousands of dollars overnight.

Common Mistakes When Estimating Stamp Duty

Small errors in your initial budget can lead to a shortfall of tens of thousands of dollars at settlement. While using a stamp duty calculator nsw provides a reliable baseline, certain variables often catch buyers off guard. Relying solely on a basic estimate without considering your specific legal structure or residency status can jeopardize your loan approval.

Buying property through a discretionary trust or a company structure often triggers the full transfer duty rate without access to individual concessions. Many investors assume they can claim first-home benefits through these entities; however, Revenue NSW rules generally restrict those savings to natural persons. If you’re planning to use a corporate entity for asset protection, you must factor in the standard rate from the outset.

Transferring a title between family members isn’t a “free” transaction. Unless the transfer results from a marriage breakdown or a specific deceased estate provision, you’ll likely pay duty on the current market value. Even if you sell a home to a sibling for A$100, Revenue NSW will assess the duty based on a professional valuation of the property’s true worth. This ensures the state receives its fair share of tax based on the asset’s actual value rather than a discounted family price.

Foreign Purchaser Surcharge Duty

Non-residents face a significant additional cost that many buyers overlook during the early planning stages. In 2026, the surcharge remains at 8% of the property value on top of the standard transfer duty. Under NSW revenue law, a “foreign person” typically includes anyone who isn’t an Australian citizen. Some permanent residents might qualify for exemptions, but they must meet strict residency tests, such as being in Australia for 200 days within the 12 months preceding the purchase.

This 8% surcharge significantly alters your borrowing capacity. Lenders include this cost in your total “funds to complete” calculation. If you haven’t budgeted for this A$64,000 extra cost on an A$800,000 apartment, your bank may reduce your loan amount at the final hour. Our team acts as your partner to ensure you calculate your total entry costs accurately before you sign a contract.

Off-the-Plan Concessions and Timing

Purchasing off-the-plan offers a unique timing benefit for owner-occupiers. You can often defer your duty payment for up to 12 months after signing the contract, or until the property settles, whichever comes first. This 12 month rule provides a helpful window to save extra funds, but it doesn’t apply to investors, who must pay within the standard three-month timeframe.

A major risk involves valuation changes between the contract date and the 2026 settlement. If the market shifts and the property’s value drops below the contract price, your lender will only lend against the lower figure. This creates a funding gap. You’ll still owe duty on the original contract price, even if the bank’s valuation is lower, so keeping a cash buffer is essential. Always double-check your figures with a stamp duty calculator nsw to stay ahead of these shifts.

Beyond the Calculator: How We Partner With You

A stamp duty calculator nsw is a helpful tool for initial planning, but it’s only the starting point of your property journey. The real work begins when we integrate that figure into a comprehensive loan structure. At Home Loan Partners, we don’t just see a tax obligation; we see a variable that affects your total borrowing capacity. We help you decide whether to use your hard-earned savings to pay the duty upfront or explore options to capitalise certain costs into the loan. This decision can be the difference between a standard interest rate and a premium one.

With access to over 36 lenders, we compare thousands of products to find the one that aligns with your specific goals. Different banks have different appetites for risk, especially regarding high LVR loans. We act as your guide, translating the dense language of credit policies into clear, actionable advice. Our focus is on your long-term security, ensuring your home loan remains sustainable long after you’ve moved in. We handle the heavy lifting so you can focus on finding the right property.

Structuring Your Loan for Maximum Efficiency

Stamp duty significantly impacts your Loan-to-Value Ratio (LVR). For instance, if you have A$150,000 saved for a A$750,000 property, your 20% deposit looks perfect on paper. However, after paying roughly A$29,000 in NSW stamp duty, your actual deposit drops to A$121,000. This pushes your LVR above 80%, which usually triggers Lenders Mortgage Insurance (LMI). This extra cost can add thousands to your total debt. We work to prevent these surprises by finding lenders with more flexible LVR thresholds or those who offer LMI waivers for certain professions. We tailor your mortgage to cover every fee, from transfer costs to registration charges, so you aren’t left short at settlement.

Your Next Steps to Property Ownership

Knowing your numbers is the first step, but securing the right loan requires a steady hand. Our expert brokers simplify the application process by managing the paperwork and negotiating directly with the banks on your behalf. We provide a personalized borrowing power assessment that reflects the current Australian lending environment. This gives you the confidence to bid at auction or make an offer knowing exactly where you stand. You don’t have to navigate these complex financial waters alone. Book a consultation with The Home Loan Partners to secure your pre-approval today and take the next certain step toward your new home.

Secure Your NSW Property Future in 2026

Navigating the property market in 2026 requires more than just a rough estimate; it demands a clear financial roadmap. Using a stamp duty calculator nsw provides a vital starting point for your budget, but these figures are only one piece of the puzzle. You’ll need to account for the latest First Home Buyer Assistance Scheme thresholds and potential concessions that could save you thousands in A$. We don’t just look at the numbers; we look at your long-term security. Our team provides expert guidance through every exemption and offers access to over 36 leading Australian lenders to find your ideal fit. Whether you’re an investor or an owner-occupier, we’ll build a tailored loan structure that protects your interests. Don’t let hidden costs or complex regulations slow your progress toward homeownership. Speak with an expert partner at The Home Loan Partners today to simplify your journey. We’re here to be your steady hand, ensuring your path to a new home is as seamless and stress-free as possible.

Frequently Asked Questions

Can I add stamp duty to my home loan in NSW?

You generally can’t add stamp duty to your home loan, as lenders expect you to pay this cost upfront using your own savings. Most banks require you to demonstrate that you have enough funds to cover both your deposit and the government’s transfer duty before they’ll offer final mortgage approval. While a few specialized lenders might allow you to borrow above the property value to cover costs, this usually triggers expensive Lenders Mortgage Insurance and increases your total debt.

How much is stamp duty on a $1 million house in NSW?

For a residential property valued at A$1,000,000 in NSW, you’ll typically pay approximately A$39,735 in transfer duty. This total includes a base rate of A$37,135 plus A$5.50 for every A$100 of value that exceeds the A$958,000 threshold. Using a stamp duty calculator nsw helps you verify these figures against current 2024 tax brackets so you can plan your purchase with total confidence.

Do first home buyers pay stamp duty in NSW in 2026?

In 2026, first home buyers will likely continue to access the First Home Buyers Assistance Scheme, which provides a full exemption on homes valued up to A$800,000. If you’re purchasing a property priced between A$800,000 and A$1,000,000, you’ll receive a sliding scale concession instead of paying the full rate. These thresholds were updated on 1 July 2023 to ensure more Australians can achieve their homeownership goals with less financial pressure.

Is stamp duty different for investment properties in NSW?

Stamp duty rates for domestic investors are the same as those for owner-occupiers in NSW. You’ll pay the standard residential rate regardless of whether you intend to live in the property or rent it out to tenants. However, if you’re a foreign purchaser, you must pay an additional 8% surcharge on top of the standard transfer duty. We’ll help you factor these costs into your investment strategy to ensure your long-term returns remain strong.

What happens if I can’t afford to pay the stamp duty at settlement?

Your property purchase cannot legally proceed if you’re unable to pay the duty by the settlement date. You’ll likely face penalty interest from the vendor, which is often set at 10% per year in standard NSW contracts, and you risk losing your entire 10% deposit if the deal falls through. Our team acts as your partner to prevent this by calculating every fee well in advance, ensuring a smooth and stress-free path to settlement.

Are there any stamp duty exemptions for pensioners in NSW?

NSW doesn’t offer a specific, broad stamp duty exemption for pensioners like some other Australian states do. Eligible pensioners can still access the Shared Equity Home Buyer Helper scheme, which launched in January 2023 for those buying homes up to A$950,000 in Sydney. This program allows the government to contribute up to 40% of the purchase price, which significantly lowers the upfront costs and ongoing mortgage repayments for older residents.

How is stamp duty calculated for vacant land intended for building?

Stamp duty is calculated based on the purchase price of the vacant land alone, provided you buy the land and the building contract separately. If you buy a block for A$500,000, you only pay duty on that amount rather than the finished value of the house, which can save you over A$10,000 in taxes. A stamp duty calculator nsw is a vital tool for construction projects, as it helps you see the clear tax benefits of building from scratch.

Do I have to pay stamp duty when refinancing my home loan?

You don’t have to pay stamp duty when you refinance an existing home loan with a new lender. The NSW government abolished mortgage duty on 1 July 2016, so switching banks to secure a better interest rate won’t trigger this tax. You’ll only need to budget for small administrative costs, such as the A$165.40 land registry discharge fee and the A$165.40 registration fee, which are standard for most Australian refinances.