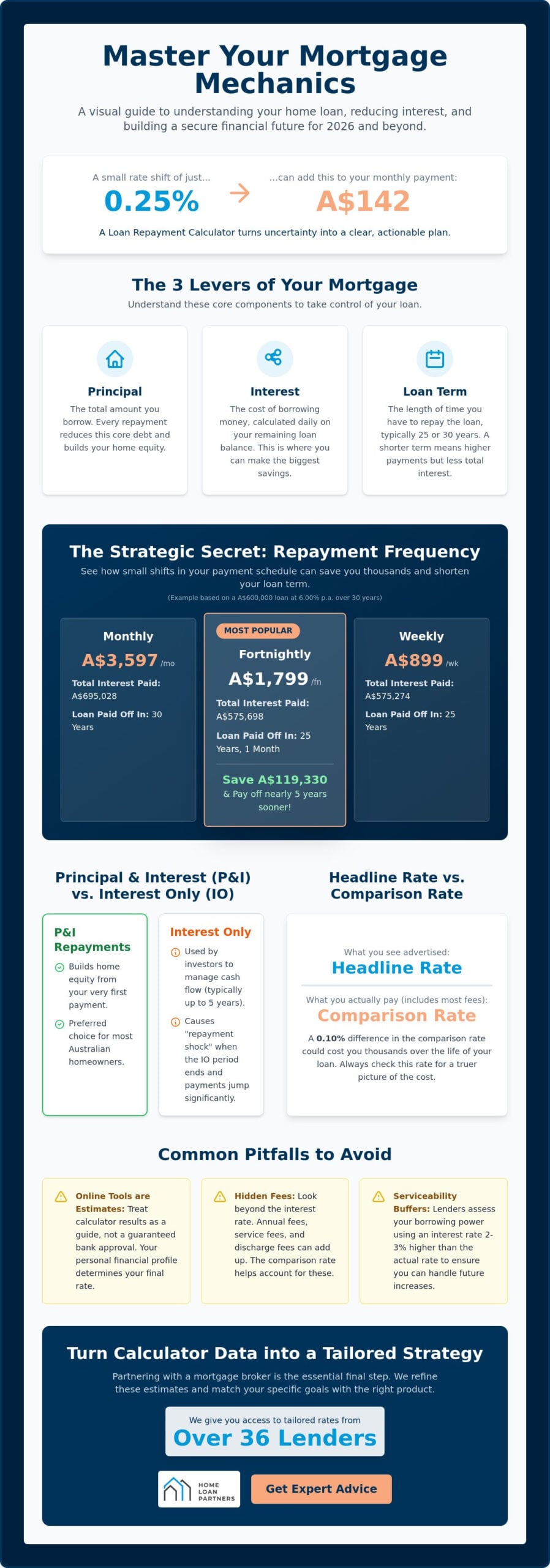

On 14 October 2025, Sarah sat at her kitchen table in Melbourne and realized that a 0.25% interest rate shift would add A$142 to her monthly commitment. It’s a common realization for many Australians as we look toward the lending environment of 2026. You likely understand that even small fluctuations in the RBA cash rate can ripple through your household budget. Using a reliable loan repayment calculator helps you move past the guesswork and see exactly how these shifts impact your bottom line.

We know that managing a mortgage often feels like a balancing act between your current lifestyle and your future freedom. You want to ensure every dollar works as hard as possible, but fear of hidden fees or complex interest calculations can make the process feel overwhelming. We’re here to help you regain control. This guide will show you how to master your mortgage mechanics and use real data to build a faster path to homeownership. We’ll break down the impact of extra repayments, explain how to factor in those elusive fees, and give you the tools to speak with your broker with total clarity about your financial future.

Key Takeaways

- Understand how to build a resilient 2026 household budget by decoding the relationship between principal, interest, and your long-term loan term.

- Learn the strategic “secret” of repayment frequency and how making small shifts in your schedule can potentially save you thousands of A$ in interest.

- Use a loan repayment calculator to transform complex mortgage variables into a clear, actionable roadmap for your Australian property journey.

- Identify common pitfalls like serviceability buffers and hidden annual fees to ensure your financial projections remain realistic and stress-free.

- Discover why partnering with a mortgage broker is the essential final step to accessing tailored rates from over 36 lenders that match your specific goals.

Why Every Property Journey Starts with a Loan Repayment Calculator

Starting your property journey in Australia requires more than just a dream; it requires a data-driven plan. A loan repayment calculator is an essential digital tool that estimates your potential mortgage costs across various frequencies. Whether you prefer to budget weekly, fortnightly, or monthly, this tool provides a baseline for your 2026 household finances. By entering variables like the loan amount, interest rate, and loan term, you gain immediate insight into your future commitments. It’s the first step in transforming a vague ambition into a structured financial reality.

Understanding how amortization calculators work is helpful for seeing how your payments are split between interest and principal over time. This early research is vital because it prevents sticker shock during the formal application process. There’s a significant difference between a basic repayment estimate and a comprehensive borrowing power assessment. While the loan repayment calculator gives you a figure based on your inputs, a full assessment considers your unique credit profile, debt-to-income ratio, and specific living expenses. Using these tools early allows you to adjust your expectations before you fall in love with a property that might sit outside your comfortable price range.

The Psychology of Budgeting for a Home

The shift from “what I want” to “what I can comfortably afford” is a major emotional milestone. Using a calculator helps you set clear savings targets for a deposit based on current market realities in cities like Sydney, Melbourne, or Brisbane. It validates your financial goals by showing you exactly how much income you need to service a specific debt level. This process replaces anxiety with a sense of control. It ensures you don’t overstretch your lifestyle, allowing you to maintain your quality of life while meeting your new obligations.

The Limitations of Online Tools

It’s vital to remember that these tools are a starting point rather than a final bank approval. Most online calculators use advertised interest rates which might not reflect the personalised rate a lender offers you based on your LVR (Loan to Value Ratio). These results should be treated as a helpful guide for your initial planning phase. At Home Loan Partners, we use these figures as a foundation for deeper, professional discussions. We’ll help you refine these estimates into a tailored strategy that accounts for the specific nuances of the Australian lending market and your long-term security.

Decoding the Variables: How Interest, Principal, and Terms Interact

Understanding your mortgage starts with three primary levers: principal, interest, and time. Your principal is the core debt, which gradually shrinks as you make repayments. Banks calculate interest daily on this declining balance, though they usually charge it to your account monthly. Using a loan repayment calculator allows you to see how a small increase in your monthly payment can significantly accelerate your equity growth. It gives you the clarity needed to decide if you should pay a little extra each fortnight.

Accuracy is vital for your long-term planning. You should always look beyond the headline rate offered in advertisements. While the headline rate is the base interest, the comparison rate includes most upfront and ongoing fees, providing a more truthful representation of the cost. For a typical A$600,000 loan, a 0.10% difference in the comparison rate could cost you thousands over the life of the loan. Tools like the Federal Student Aid Loan Simulator demonstrate how different variables change the total cost of debt, providing a clear perspective on how structured repayments work over time.

Principal and Interest (P&I) vs. Interest Only

P&I repayments are the preferred choice for most Australian homeowners because they build equity from day one. You aren’t just paying for the right to live in the house; you’re owning more of it every month. Investors often choose interest-only periods, typically capped at 5 years, to maximize tax benefits or manage short-term cash flow. However, once that period ends, repayments jump significantly because you must pay off the full principal over a shorter remaining term. This “repayment shock” can be stressful if you haven’t discussed a tailored refinancing strategy with a partner who understands your goals.

The Impact of the Loan Term on Your Total Interest

The loan term is the primary driver of the total interest cost over the life of your mortgage. While a 30-year term is the standard in the Australian market, choosing a 25-year term can be a powerful wealth-building move. On an A$500,000 loan at a 6.00% interest rate, shifting from a 30-year to a 25-year term increases monthly repayments by roughly A$225. However, this simple change saves you over A$100,000 in total interest charges. It’s a direct trade-off between your current monthly cash flow and your future financial freedom. Using a loan repayment calculator to compare these two scenarios helps you find the “sweet spot” where your budget remains comfortable while your debt disappears faster.

Beyond the Minimum: Strategies to Reduce Your Total Interest Bill

While your lender sets a minimum monthly figure, sticking strictly to that schedule is often the most expensive way to own your home. By using a loan repayment calculator to model different scenarios, you can see how small adjustments to your strategy today create massive savings over the next 30 years. Our goal as your mortgage partner is to help you build equity faster and keep more of your hard-earned money in your pocket. These strategies aren’t about making radical lifestyle sacrifices; they’re about making the banking system work for you rather than against you.

Repayment Frequency: Making the Calendar Work for You

Switching from monthly to fortnightly repayments is one of the simplest ways to shave years off your loan. There are 12 months in a year, but 26 fortnights. By paying half your monthly amount every two weeks, you effectively make 13 full monthly payments every calendar year. This “hidden” extra payment happens automatically without you needing to find extra room in your monthly budget. On a A$600,000 loan balance at a 6% interest rate, this single change can save you over A$105,000 in interest and reduce your loan term by roughly four years. Aligning these payments with your pay cycle makes budgeting seamless and ensures you’re constantly chipping away at the principal balance.

The Role of Offset Accounts and Redraw Facilities

An offset account functions as a high-interest savings vehicle that sits alongside your mortgage. Every dollar in this account “cancels out” an equivalent dollar of debt for interest calculations. If you have a A$600,000 loan and keep A$50,000 in your offset, the bank only charges interest on A$550,000. This keeps your cash accessible for emergencies while providing a “return” equal to your mortgage interest rate. You can use a loan payment calculator to visualize how consistent deposits into an offset account drastically alter your total interest bill over time.

The mathematical power of early extra repayments is significant because interest is calculated daily. Every extra dollar you contribute in the first five years of your mortgage does more heavy lifting than a dollar contributed in year 25. While an offset account offers flexibility, a redraw facility allows you to pull back extra repayments you’ve made directly into the loan account. Deciding which tool fits your life depends on your spending habits and future plans. You can explore the specific pros and cons in our guide on Redraw vs Offset Account: Which Is Better For You? to find the right fit for your household.

- Consistency: Even an extra A$50 per week can save tens of thousands in interest.

- Accessibility: Offset accounts provide liquidity that direct repayments don’t always offer.

- Timing: Using a loan repayment calculator shows that the earlier you start, the greater the compounding benefit.

Common Pitfalls to Avoid When Estimating Your Mortgage Costs

A loan repayment calculator provides a solid foundation for your property journey, but relying solely on a basic output can lead to unexpected financial strain. Real-world lending involves layers of costs that automated tools frequently overlook. To protect your future home security, you must account for the hidden variables that banks use behind the scenes to assess your eligibility.

One primary oversight is the serviceability buffer. While you might see a market rate of 6.15%, Australian regulators like APRA require banks to assess your ability to pay at a rate 3% higher than the current offer. This means your application is tested against a hypothetical 9.15% interest rate to ensure you can handle future fluctuations. Beyond interest, ongoing costs like annual package fees, which often sit around A$395 per year, or monthly service charges of A$10 to A$15, can quietly erode your monthly budget if they aren’t factored into your initial estimates.

Be cautious of introductory rates or honeymoon periods. These offers might feature a lower rate for the first 12 to 24 months, but your repayments will jump significantly once that period ends. If you’re opting for a variable loan, even a small 0.25% increase in the cash rate can add hundreds of dollars to your annual costs. Preparing for these shifts now prevents stress later in the life of your loan.

Accounting for Lenders Mortgage Insurance (LMI)

If your deposit is less than 20% of the property value, you’ll likely face Lenders Mortgage Insurance. This isn’t a small fee; it’s a significant cost that can reach A$15,000 or more on a standard home loan. Most basic calculators exclude the LMI premium, which is often capitalised into the loan, increasing your total debt and interest charges. We often help clients explore professional structuring or family guarantee options to minimise or entirely avoid this expense, keeping more equity in your pocket from day one.

The Importance of a Buffer in Your Personal Budget

A serviceability buffer is the safety net required by Australian regulators to ensure borrowers can withstand economic shifts. While the bank applies their own 3% test, we recommend you personally use a loan repayment calculator to test your budget at a rate at least 2% higher than today’s best offer. This proactive approach builds a worst-case scenario into your lifestyle planning. It ensures your home remains a sanctuary rather than a source of pressure if the market shifts. Beyond your repayments, it’s equally important to account for upfront government costs — buyers purchasing in New South Wales can use a stamp duty calculator NSW to estimate transfer duty and identify potential first-home buyer concessions before committing to a purchase. Our team can help you partner with an expert advisor to build a tailored strategy that accounts for every hidden cost, ensuring your path to homeownership is both transparent and secure.

Turning Calculator Data into a Tailored Home Loan Strategy

While a loan repayment calculator offers a helpful starting point, it can’t account for the subtle nuances of your specific financial situation. Online tools provide a generic snapshot of what your monthly commitments might look like in 2026, but they lack the context of lender-specific credit policies and the evolving Australian regulatory environment. Moving from a digital estimate to a signed contract requires a bridge between raw data and a personalized strategy.

We act as that essential bridge. Our team provides direct access to more than 36 lenders across Australia, ranging from the major banks to specialized boutique providers. This variety is vital because a calculator often uses a standard interest rate that might not reflect the best offer available for your specific credit profile. We identify the products where your income, deposit size, and long-term goals align with a lender’s criteria. This ensures the numbers you saw on your screen actually translate into a real-world approval.

The transition from “online research” to “keys in hand” is rarely a straight line. By adopting a partner approach, we move you away from generic estimates and toward a settled mortgage that fits your life. We don’t just find you a loan; we manage the entire trajectory to ensure your property journey is as smooth as possible.

How The Home Loan Partners Refine Your Results

We look past the headline interest rate to find a loan structure that supports your future security. Whether you’re a first home buyer navigating the market for the first time or an investor looking to maximize equity, the right structure is just as important as the rate. We help you determine if features like offset accounts or redraw facilities will save you money based on your actual cash flow habits.

Our experts handle the heavy lifting with the banks. We manage the complex paperwork, clarify the technical jargon, and negotiate on your behalf to secure competitive terms. This supportive approach removes the inherent stress of the mortgage process. For first home buyers, we provide a protective layer of guidance to ensure you’re making informed decisions at every milestone.

Ready to See Your Real Numbers?

Stop guessing and start planning with absolute certainty. A professional assessment takes your loan repayment calculator estimates and turns them into a formal pre-approval. This gives you the confidence to bid at auction or make an offer, knowing exactly where you stand with the banks. It’s the difference between a rough idea and a concrete plan.

Book a consultation today to turn your property aspirations into a reality. We’re here to guide you through the entire journey, from your first enquiry to the day you settle and throughout the life of your loan.

Your Roadmap to a Smarter Mortgage Strategy

Navigating the Australian property market in 2026 requires more than just a deposit; it demands a clear understanding of how your debt behaves over time. By utilizing a loan repayment calculator, you’ve already taken the most important step in decoding how interest rates and loan terms impact your weekly budget. You now understand that even small additional repayments can significantly reduce a standard 30 year loan term, potentially saving you thousands in interest charges. Avoiding common estimation errors ensures your financial foundation remains solid as market conditions evolve.

Data is powerful, but it’s only the beginning of your journey. At Home Loan Partners, we act as your expert guide to turn these calculations into a living strategy. We provide access to over 36 lenders to ensure your loan structure matches your specific life goals, whether you’re a first home buyer or a seasoned investor. We believe in a personalized financial partnership that lasts well beyond your settlement date. Let us find the right loan structure for your goals and help you secure your piece of the Australian dream with confidence and ease.

Frequently Asked Questions

Is a loan repayment calculator accurate?

A loan repayment calculator provides a highly accurate mathematical estimate based on the data you provide. It calculates your scheduled payments using the loan amount, term, and interest rate. However, it can’t predict future RBA cash rate shifts or specific bank margin changes. For a 30 year term, use it as a guiding tool to understand your baseline commitments before we tailor a specific plan for your household budget.

Does an offset account reduce my actual monthly repayment amount?

An offset account typically doesn’t lower your required monthly bank transfer. Instead, it reduces the interest charged on your balance, meaning more of your payment goes toward the principal. If you hold A$50,000 in an offset against a A$500,000 mortgage, the bank only charges interest on A$450,000. This helps you pay off the debt years earlier without changing your lifestyle or monthly cash flow.

What is the difference between a mortgage calculator and a borrowing power calculator?

These tools serve two distinct roles in your property journey. A borrowing power calculator estimates the total amount a lender might give you based on your income and the Household Expenditure Measure (HEM). Conversely, a loan repayment calculator shows what that debt actually costs you every month. We use both to ensure your dream home aligns with a comfortable daily reality for your family.

How much extra should I pay off my mortgage each month to save 5 years?

The exact amount depends on your loan balance and current interest rate. On a standard A$600,000 mortgage at a 6.0% interest rate, contributing an extra A$450 per month can shorten your 30 year term by 5 years. This strategy could save you over A$140,000 in total interest costs. Small, consistent additions are the most effective way to build equity and secure your financial freedom sooner.

Can I use a loan repayment calculator for an investment property?

Yes, you can use these tools for investment properties, though you’ll need to adjust the variables. Investment interest rates are often 0.5% to 1.0% higher than owner-occupied rates. Since 65% of Australian investors choose interest-only periods for tax purposes, ensure you toggle the calculator settings to reflect those specific payment structures. This helps you accurately forecast the net rental yield and cash flow.

What interest rate should I put into the calculator for a realistic 2026 estimate?

For a realistic 2026 outlook, we recommend using a rate between 6.5% and 7.5%. While market forecasts vary, Australian lenders currently apply a 3.0% serviceability buffer above their floor rates to ensure you can handle future fluctuations. Modelling your repayments at these higher levels provides a safety net. It ensures your mortgage remains manageable even if the economic environment shifts unexpectedly during your loan term.

Are bank fees included in the repayment calculation?

Standard calculators generally don’t include ongoing bank fees in their primary results. You should account for an additional A$10 to A$15 for monthly service fees or approximately A$395 for annual package fees depending on your lender. While these numbers seem small, they add up over a 30 year period. We’ll help you factor these costs into your total budget so there aren’t any surprises at settlement.

How does a change in interest rates affect my monthly repayments?

When interest rates rise, your monthly repayment increases because the interest component of your debt becomes more expensive. For a A$500,000 loan balance, a 0.25% increase in the interest rate typically adds about A$80 to your monthly payment. Understanding this relationship helps you prepare for volatility. We act as your partner to monitor these changes and identify when it’s the right time to fix your rate or refinance.